Giving money or assets away during your lifetime is one of the simplest ways to reduce a future Inheritance Tax (IHT) bill. Many people do not realise, however, that a gift can still count towards your estate for up to seven years. If you die within that window, your family could face an unexpected tax bill. A Gift Inter Vivos policy is designed to solve exactly that problem.

Most gifts you make to another person are treated as a Potentially Exempt Transfer (PET). If you survive for seven years after making the gift, it falls completely outside your estate and there is no IHT to pay on it.

Some gifts are exempt straight away and don't start the seven-year clock at all, including:

Gifts above these allowances are PETs, and that's where the seven-year rule comes in.

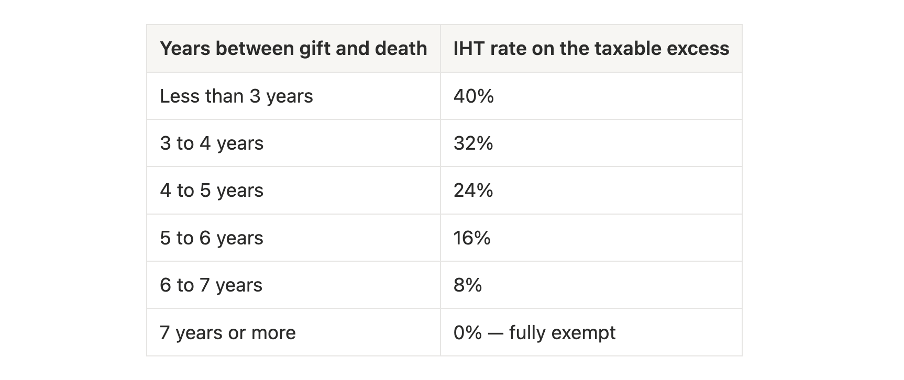

If you die within seven years of making a gift, its value is added back into your estate when your IHT is calculated. Gifts use up your nil-rate band (currently £325,000) first, and anything above that is potentially taxable at the standard IHT rate of 40%.

In other words, the gift you thought was "given away" can still create a tax liability, and it is usually the person who received the gift who becomes responsible for the tax on it.

If you survive at least three years, taper relief can reduce the amount of tax due. Crucially, taper relief reduces the tax payable, not the value of the gift, and it only applies to gifts that exceed the nil-rate band.

A Gift Inter Vivos policy is a life assurance policy designed for one purpose: to provide a lump sum to cover the potential IHT liability if the donor (person making the gift) dies within seven years of making a gift.

Its key features make it a neat fit for this risk:

In short, it turns an uncertain, potentially large tax bill into a modest, predictable cost, while protecting the value of the gift you intended to pass on.

The real appeal is how little this peace of mind costs relative to the size of the gift being protected. The figures below are based on £1m of single life cover protecting a £2.5m gift, with premiums reducing each year in line with taper relief.

For a younger or middle-aged donor, the cost of fully protecting a gift can be a fraction of 1% of its value, which is a small price to remove a potential 40% tax risk for your family.

💡 A note on the nil-rate band: because a gift uses up your nil-rate band first, the portion that falls within the £325,000 band effectively pushes an equivalent slice of your remaining estate into the taxable bracket, where it is charged at 40%. Taper relief offers no help here, as it only applies to the value above the nil-rate band. To cover this, a separate level term policy can be put in place for the full seven years, sized to that additional liability, staying level rather than reducing, precisely because this part of the bill doesn't taper away.

Gifting is a powerful way to pass wealth to the next generation, but the seven-year rule means timing and planning matter. A Gift Inter Vivos policy bridges the gap, making sure that an early death doesn't leave your loved ones with a tax bill they weren't expecting, and your gift retains it value and can help your loved ones as intended.

Thinking about making a significant gift? We can help you understand your potential IHT exposure and whether Gift Inter Vivos cover is right for you. Get in touch to arrange a conversation.

This article is for general information only and does not constitute financial advice. Tax treatment depends on individual circumstances and may change in the future. Premium figures are illustrative and sourced from JLHO Gift Cover rates (January 2026).