The ongoing war in the Middle East has undoubtedly caused a ripple effect throughout global markets. Oil prices have spiked, perhaps surprising, gold prices have fallen from their January peak, and markets hang on every word (or Truth Social message) the US president says.

One impact now priced into UK markets is an expectation that interest rates will rise over the next 12 months. This of course will impact borrowers and savers alike, but how can you make the most of this change?

When interest rates are attractive, it is natural to leave surplus money in an interest‑earning bank account. The challenge for higher and additional-rate taxpayers is that bank interest is taxed as income, which can significantly reduce the net return.

A useful alternative that we often recommend at Investment Quorum is investing in low-coupon UK government gilts. These are UK government bonds where the majority of the investor’s return comes from the bonds price gradually increasing to maturity, rather than from a large interest (coupon) payment. That matters because, for UK individual investors, capital gains on gilts are generally exempt from Capital Gains Tax (CGT), while coupon interest is taxable as income.

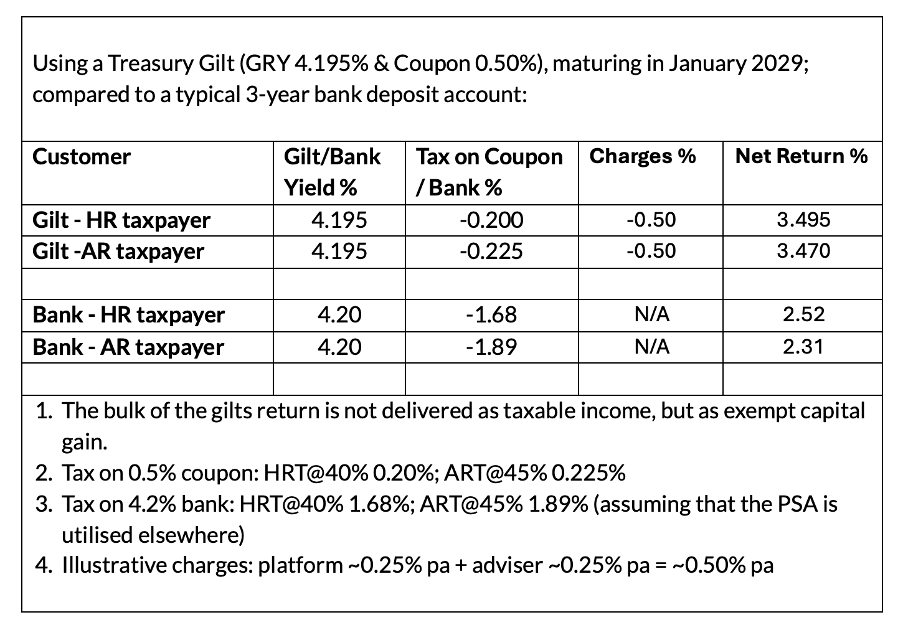

The result is that investors can see a higher net return from their surplus cash from gilts than from standard deposit accounts. The differences are broken down below:

You may benefit from reduced rates of tax via the Personal Savings Allowance (PSA), but it is limited (and for additional-rate taxpayers it is effectively nil). Once the PSA is used, interest is taxed at the individual’s marginal rate (i.e. 20%, 40% or 45%).

The return is typically split into:

That means a large portion of the overall yield can be economically similar to interest but treated more favourably for tax.

For many taxpayers, the real comparison is not ‘headline savings rate vs gilt yield’. It is instead ‘net return of cash vs net return of gilts’.

This is why low-coupon gilts often look most compelling when:

Low-coupon gilts are not risk-free in every sense, but they have distinct characteristics:

Based on these figures, the gilt provides an estimated net return around 3.495% p.a., versus cash around 2.5% p.a. for a higher-rate taxpayer, primarily because the bulk of the gilt’s return is not delivered as taxable income.

Low-coupon gilts can be particularly attractive when:

They may be less suitable when:

For higher and additional-rate taxpayers, the tax treatment is often the deciding factor when considering holding cash or gilts. The tax treatment will materially change the net outcome, even if the headline rates look similar.

Note: Tax treatment depends on individual circumstances and can change. Any decision should be confirmed against the investor’s tax position and the specific dealing/holding structure.